Official Site of The State of New Jersey

Official Site of The State of New JerseyBest Practices for New Jersey Local Governments Using Coronavirus Local Fiscal Recovery Funds

Update (February 2022): The information in this documentation or presentation pertains to the Interim Final Rule, which is in effect until April 1, 2022. The Final Rule, effective April 1, 2022, can be found here.

The American Rescue Plan Act of 2021 (ARPA) is a $1.9 trillion economic stimulus bill signed by President Biden on March 11, 2021 to provide funding for COVID-19 response and recovery. Within the ARPA, the Coronavirus Local Fiscal Recovery Fund (Local Fiscal Recovery Funds) allocates funding for all counties and municipalities in the State of New Jersey. Counties and metropolitan cities (as defined in the ARPA) will receive this funding directly. Municipalities with populations of less than 50,000 (or “non-entitlement units”) will receive the funding through the State. New Jersey municipalities and counties have been allocated $3.6 billion in Local Fiscal Recovery Funds.

The Office of State Comptroller (OSC) was created in 2007 as an independent agency that oversees and audits state agencies, independent state authorities, state colleges and universities, local governments, and boards of education and reviews and monitors procurements by those entities. OSC investigates allegations of fraud, waste, and abuse in the expenditure of public funds, promotes efficiency, identifies cost savings, and detects and prevents misconduct at all levels of government. Pursuant to N.J.S.A. 52:15C-15, OSC is charged with providing technical assistance and training regarding best practices for developing and implementing financial management systems, establishing effective internal controls, and preventing the misuse of public funds. Consistent with that authority, this document is intended to be a resource for New Jersey’s local government units charged with administering the ARPA’s Local Fiscal Recovery Funds.

Comply with Applicable Guidance

The U.S. Department of Treasury (U.S. Treasury) issued an interim final rule[1] implementing the Local Fiscal Recovery Funds under the ARPA and outlining how local governments can use Local Fiscal Recovery Funds. U.S. Treasury also published general FAQs, FAQs related specifically to non-entitlement units, Compliance and Reporting Guidance, and a quick reference guide that provides further details regarding use of the funds. Because these resources are updated regularly, local governments should be sure to review U.S. Treasury’s website for the most up-to-date information and sign up to receive email updates using the “Receive COVID-19 Relief Updates” button.

The U.S. Treasury guidance should be read in concert with the award terms and conditions and other applicable regulatory and statutory requirements, including the Uniform Guidance (2 CFR Part 200), which is an authoritative set of requirements for expending federal funds. Most of the provisions of the Uniform Guidance apply to Local Fiscal Recovery Funds, including the Cost Principles and Single Audit Act requirements.

Local governments should refer to the Assistance Listings for detail on the specific provisions of the Uniform Guidance that do and do not apply. To access this information, search for Assistance Listing Number (ALN) 21.027 (formerly known as CFDA number) on the Assistance Listings webpage and review the section on “Compliance Requirements.”[2] It is important that local governments comply with these requirements in order to ensure that money is spent properly, without fraud, waste, and abuse, and is not subject to recoupment in the future due to non-compliance. Local governments that are unfamiliar with the Uniform Guidance should consider training or consulting with experts to ensure their compliance.

To supplement U.S. Treasury guidance related to Local Fiscal Recovery Funds, the New Jersey Division of Local Government Services (DLGS) issued Local Finance Notice (LFN) No. 2021-11, which describes the permitted and prohibited uses of the Local Fiscal Recovery Funds. It also addresses issues such as duplication of benefits, reporting requirements, and budgeting and recording receipts.

Local government units should consult the resources listed above, as well as legal counsel or subject matter experts, for assistance in determining whether a proposed use of Local Fiscal Recovery Funds is eligible.

Best Practices

- Review the ARPA, U.S. Treasury Guidance, Uniform Guidance, and other guidance documents to ensure compliance with eligible uses.

- Review the Local Finance Notice and any other applicable guidance from the Division of Local Government Services.

- Consult with legal counsel or subject matter experts or attend training, if necessary, to understand applicable requirements.

Take Time to Plan

Local Fiscal Recovery Fund recipients may use the funds to cover eligible costs incurred between March 3, 2021 and December 31, 2024, provided that the obligations incurred are expended by December 31, 2026. Any unused funds must be returned to U.S. Treasury. The timeframe to incur and expend funds allows local governments time to plan for their use of the funds.

As a best practice, OSC recommends that local governments invest time in engaging with the community and other stakeholders to assess community needs, determine priorities, and analyze potential costs to ensure that funds are used efficiently and advance shared interests in the community. Planning should involve consideration by the local government of how the funding will be used to promote equitable delivery of government benefits and opportunities to underserved communities, as outlined in Executive Order 13985, Advancing Racial Equity and Support for Underserved Communities Through the Federal Government.

When engaging in planning, local governments should take into account other funding streams under the ARPA and other federal or state assistance programs in order to coordinate their response to the pandemic and its economic effects. Coordination and communication among governmental and non-profit partners is crucial to ensure that benefits are not duplicated, resources are used efficiently, and the impact of federal and state assistance is maximized. Local units should ensure they comply with LFN No. 2021-11, which requires that they share information on new programs with the Department of Community Affairs to determine whether a duplication of benefits has occurred or may occur.

As noted in LFN No. 2021-11, local governments should collaborate with state, regional, or local entities on certain initiatives to share or reduce administrative and other burdens. For example, local governments may use resources and programmatic infrastructure already available from other local and state efforts.

Best Practices

- Engage with constituents and stakeholders to assess community needs, priorities, and costs to ensure funds are used effectively.

- Consider how funding will be used to promote equitable delivery of government benefits and opportunities to underserved communities.

- Communicate with state, local, and non-profit partners to ensure funding and efforts are not duplicated. Provide information on new programs to the Department of Community Affairs to check for potential duplication of benefits.

- Consider collaborating with state, regional, or local entities to help distribute funds or administer programs more efficiently.

Plan for a Successful Procurement

The key to a successful procurement is proper planning. A local government that intends to use Local Fiscal Recovery Funds for eligible projects should develop a realistic timeline for public bidding. Local governments are reminded that projects expected to exceed $12.5 million must be submitted to OSC for review at least 30 days prior to advertisement as required by N.J.S.A. 52:15C-10(b). For contracts valued at $2.5 million or more, but less than $12.5 million, local governments are required to notify OSC within twenty business days after the award has been made. More information regarding submission of contracts for review by OSC may be found on OSC’s website.

Generally, to ensure compliance with the federal procurement requirements, local governments should use the procurement methods authorized under the Local Public Contracts Law (LPCL), N.J.S.A. 40A:11-1 et seq., for all contracts funded with Local Fiscal Recovery Funds, subject to any additional restrictions and requirements in 2 CFR 200.318-200.327. Local units should also ensure that they comply with the terms and conditions of their funding agreement. Prior to issuing any bid for projects that are federally funded, local governments should carefully review their bid documents to make sure that all federally required contract provisions have been included. A list of the federally required contract provisions can be found at 2 CFR 200 Appendix II.

For example, all federally funded contracts must now include a provision regarding a preference for the purchase, acquisition, or use of domestically produced goods. See 2 CFR 200.322. Local units should also be mindful that pursuant to 2 CFR 200.216, recipients and subrecipients of federal funds are prohibited from obligating or expending loan or grant funds to purchase covered telecommunications equipment from certain companies. These contracts must also include provisions requiring compliance with the Contract Work Hours and Safety Standards Act and ensure that a contract award is not made to a party that has been debarred or suspended in the federal System for Award Management (SAM). Failure to include and enforce these specific terms and conditions within contracts funded with Local Fiscal Recovery Funds may result in recapture of funds. Finally, while the SLRF does not require compliance with the Davis Bacon Act, local units are reminded that compliance with the New Jersey Prevailing Wage Act is still required. (Updated 12/21)

Local units should be aware that federal procurement regulations strongly disfavor the use of time and materials contracts. Avoidance of time and material contracts is recommended in all circumstances involving federal funding. Additionally, if a firm assists in the development or drafting of specifications, that firm must be excluded from competing for the resulting procurement in accordance with 2 CFR 200.319(b).

Local units must ensure they maintain adequate records of procurements to guarantee compliance with applicable reporting and record retention requirements for Local Fiscal Recovery Funds and establish written standards regarding conflicts of interest pursuant to 2 CFR 200.318.

Finally, local governments should only award contracts under the public exigency exception of the LPCL when conditions affecting the public health, safety or welfare require the immediate delivery of goods or the performance of services. Strict adherence to the statutory requirements governing emergency purchases set forth in N.J.S.A. 40A:11-6 and regulations at N.J.A.C. 5:34-6.1 is essential.

Best Practices

- Comply with the procurement methods of the LPCL in order to ensure compliance with the full and open competition requirements of the federal procurement regulations for all contracts funded with Local Fiscal Recovery Funds.

- Include all federally required contract provisions in contracts funded with Local Fiscal Recovery Funds. These can be found at 2 CFR Part 200 Appendix II.

- Avoid time and material contracts.

- Do not allow firms that assist in the development of specifications to be considered for award of the resulting contract.

- Maintain adequate records of each procurement funded with Local Fiscal Recovery Funds to comply with reporting and record retention policies to avoid recapture of funds.

- Maintain written conflict of interest standards.

- Remember, poor planning does not constitute an emergency.

Establish Proper Internal Controls

Internal controls are defined in 2 CFR 200.1 as processes designed and implemented to provide reasonable assurance that the following objectives are achieved: (1) effectiveness and efficiency of operations; (2) reliability of reporting for internal and external use; and (3) compliance with applicable laws and regulations.

As required by 2 CFR 200.303, local governments that have received federal funding, such as Local Fiscal Recovery Funds, must establish and maintain effective internal controls that provide reasonable assurance that the local governments are managing the federal funds in compliance with all applicable federal statutes, regulations, and the terms and conditions of the federal award.

Internal controls should be in compliance with one of two approved frameworks:

- the Government Accountability Office (GAO) Standards for Internal Control in the Federal Government (commonly called “the Green Book”) or

- the Committee of Sponsoring Organizations of the Treadway Commission (COSO) framework.

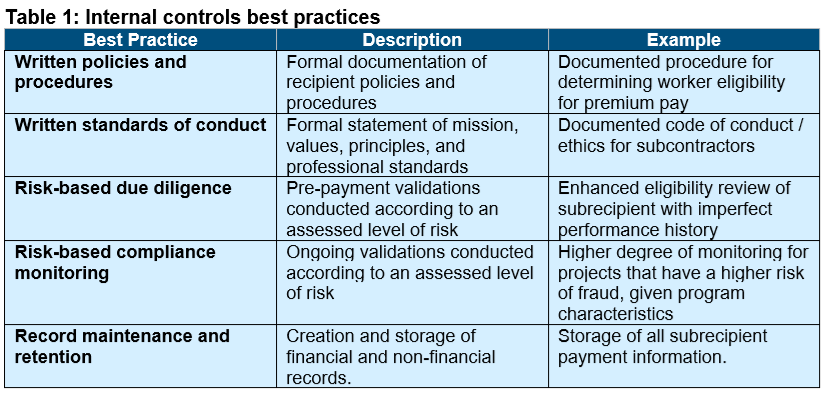

In the table below, provided in U.S. Treasury’s Compliance and Reporting Guidance, U.S. Treasury describes some best practices for development of internal controls:

OSC has developed a self-assessment internal controls checklist for local government units to use to assess their own internal control environment and determine whether internal controls are in place or whether internal control weaknesses exist. The checklist serves as a basic template to evaluate internal controls, but it is important that internal control checklists are tailored, as required, to the specific needs of local governments. Local governments should also review prior audits and consult independent auditors to identify any risks and concerns related to their internal control environment.

Best Practices

- Review internal controls to ensure they are adequate to comply with the GAO’s Green Book or COSO standards.

- Consult prior audits or independent auditors for any risks or concerns related to the current internal control environment.

- Use OSC’s Internal Control Checklist for Local Governments to assess internal controls and identify potential weaknesses.

Assess Programmatic and Organizational Risk

New funding and new programs create new risks. Local governments should assess risk related to the entity as a whole and at a programmatic level to identify opportunities for fraud, waste, abuse, or mismanagement of funding. In order to oversee and manage funds effectively, local governments should conduct and document written risk assessments to identify potential risk factors and evaluate whether it is necessary to modify existing internal controls or institute new internal controls in order to control or mitigate identified risks. Risk assessments should be completed and updated on an ongoing basis to ensure proper oversight.

Due to the COVID-19 pandemic, new risks of fraud, waste, or abuse may arise based on factors such as:

- Remote or hybrid work environments

- Substantial increases in funding amounts

- Compliance with new regulations and guidance

- Inexperience with federal reporting or grants management

- Less transparency or oversight since public meetings are not in person and responses to public records requests may be delayed

- Desire to disseminate funding quickly to meet immediate needs

- Staff handling new or additional responsibilities

- Reliance on service providers or temporary workers

- Differing documentation requirements due to remote settings (e.g. electronic signatures/ documents)

- Data security or privacy concerns

- Public safety and public health concerns

For more information on conducting fraud risk assessments, see the COVID-19 Compliance Plan and the Risk Assessment Template, available on OSC’s website.

Best Practices

- Conduct written risk assessments of the organization and its programs.

- Take steps, such as updating internal controls, to mitigate any identified risks.

Allocate Appropriate Staffing

Additional funding may create additional administrative and other burdens on local and state governments. From processing disbursements, managing new contracts, planning investments, creating program guidelines, and reviewing applications, to managing documentation and reporting requirements, this additional funding may strain public employees. Insufficient staffing may hamper efforts to disburse funding efficiently and to provide appropriate oversight. As a best practice, entities should review staffing to ensure that sufficient, qualified staff are allocated to Local Fiscal Recovery Fund projects. Additionally, if necessary, local governments should provide training to existing staff to ensure they are qualified to meet new responsibilities and obligations.

Local governments should be aware that Local Fiscal Recovery Funds may be eligible to be used for certain administrative costs (e.g. payroll and benefits costs) of employees performing administrative work related to the COVID-19 public health emergency and its related economic impacts. This may include costs related to disbursing Local Fiscal Recovery Funds and managing new grant programs established using Local Fiscal Recovery Funds. It may also include costs of consultants to support effective management and oversight, including consultation for ensuring compliance with legal, regulatory, and other requirements.

Best Practices

- Review staffing plans to ensure adequate, qualified staff dedicated to administering and tracking funding and managing new and existing programs.

- Consider investing time and resources to training staff on new requirements.

- Keep in mind certain administrative costs may be eligible for reimbursement using Local Fiscal Recovery Funds.

Collect and Maintain Proper Documentation

Local government entities should plan ahead to ensure they are collecting and maintaining appropriate documentation to support expenditures using Local Fiscal Recovery Funds. Financial records and supporting documents related to the award must be retained for period of five years after all funds have been expended or returned to U.S. Treasury, whichever is later. Local governments should consult U.S. Treasury guidance for specific documentation requirements related to Local Fiscal Recovery Funds, as well as their Financial Assistance Agreement to ensure compliance with its terms. Local governments should also comply with local and state record retention policies, which may have longer retention periods.

Best Practice

- Maintain documentation for 5 years after all Local Fiscal Recovery Funds have been spent.

- Consult applicable record retention laws, regulations, and policies, including the Destruction of Public Records Law, N.J.S.A. 47:3-15 et seq., to determine whether longer retention periods are required.

Prepare to Meet Reporting Requirements

The U.S. Treasury Compliance and Reporting Guidance provides detailed information related to the reporting requirements for the Local Fiscal Recovery Funds. U.S. Treasury will issue a User Guide and other reference materials before reporting deadlines with additional information on how to submit reporting.

In general, there are three types of reporting for these funds that may be required, depending on recipient type:

- Interim Report: An initial overview of status and uses of funding. This is a one-time report.

- Project and Expenditure Report: A report on projects funded, expenditures, and contracts and subawards over $50,000, and other information.

- Recovery Plan Performance Report: The Recovery Plan Performance Report (the “Recovery Plan”) will provide information on the projects that large recipients are undertaking with program funding and how they plan to ensure program outcomes are achieved in an effective, efficient, and equitable manner. It will include key performance indicators identified by the recipient and some mandatory indicators identified by U.S. Treasury. It must be posted on the website of the recipient as well as provided to U.S. Treasury.

Local governments should review the U.S. Treasury Compliance and Reporting Guidance in detail to determine what reporting is required and when the reports will be due. Local units that have not previously produced such reports should plan ahead to ensure adequate time is set aside to complete reports and troubleshoot any issues.

Best Practices

- Be aware of the applicable reporting requirements and deadlines.

- Plan ahead to ensure adequate time to comply with all reporting requirements.

Comply with Single Audit Requirements

Local government units that expend more than $750,000 in federal awards during their fiscal year will be subject to an audit under the Single Audit Act and its implementing regulation at 2 CFR Part 200, Subpart F regarding audit requirements. Examples and single audit submissions can be found at the Federal Audit Clearinghouse.

Best Practice

- Review the responsibilities under the Single Audit Act and 2 CFR Part 200 regarding audit requirements.

Engage in Subrecipient Monitoring

Local governments are permitted to pass along Local Fiscal Recovery Funds for eligible uses to third parties such as individuals, authorities, fire districts, boards of education, nonprofits, and small businesses. However, the local government will be responsible for ensuring that subrecipients adhere to federal requirements. Pass-through entities are required to manage and monitor their subrecipients to ensure compliance with requirements of the award pursuant to 2 CFR 200.332. Local governments should review the U.S. Treasury Compliance and Reporting Guidance for additional information on applicable requirements.

Best Practice

- Review applicable state and federal laws and regulations, including those set forth in 2 CFR 200.332 and U.S. Treasury Compliance and Reporting Guidance to ensure requirements are fulfilled as a pass-through entity.

Apply Lessons Learned from the CARES Act and Prior Disaster Recovery Efforts

When the CARES Act was enacted in March 2020, governments were under pressure to spend the funding expeditiously and disseminate funds quickly to individuals and businesses that urgently needed assistance. Now, over a year later, with this next round of funding, local governments should assess their performance, especially in areas in which they have faced challenges. Local governments should balance the need to meet urgent community needs with the need to implement appropriate controls, avoid fraud, waste, and abuse, and maintain required documentation and data.

The U.S. Treasury Office of Inspector General and Pandemic Response Accountability Committee provide links on their websites to reports and relevant audits and investigations related to the use of federal COVID-19 funding. Local governments can review these reports for insights into prior issues and audit findings, and to identify potential areas of concern in their own programs.

Best Practices

- Review U.S. Treasury Office of Inspector General and Pandemic Response Accountability Committee reports to apply lessons learned from the CARES Act and prior disaster efforts.

- Develop clear program guidelines from the outset.

- Ensure proper documentation requirements to prevent and deter fraud, waste, and abuse.

- Segregate accounts and properly track and document expenditures.

- Maintain complete and accurate data.

Managing New Relief Programs

Local governments may wish to use Local Fiscal Recovery Funds to directly assist residents and businesses impacted by the COVID-19 pandemic by providing funding for rental or mortgage assistance, direct payments, or other assistance. Some local governments may have limited experience in establishing and managing such programs. These government units should keep in mind the following list of best practices.

Best Practices

- Establish clear program guidelines and eligibility requirements.

- Create proper internal policies and procedures.

- Collect and maintain appropriate documentation from applicants.

- Disburse funds efficiently.

- Advertise programs fairly and effectively.

- Collaborate with other state and local partners to share information/resources and ensure no duplication of benefits exists.

- Develop appropriate legal agreements for disbursements.

- Ensure civil rights compliance by meeting legal requirements relating to nondiscrimination and nondiscriminatory use of federal funds.

Reporting Fraud, Waste, and Abuse

If you have any information about the fraud, waste, or abuse of Local Fiscal Recovery Funds or other COVID-19 relief funds, you can contact the New Jersey Office of the State Comptroller through the online complaint form, by email at ComptrollerTips@osc.nj.gov, or by calling the toll-free hotline, 1-855-OSC-TIPS.

Resources:

[1] U.S. Treasury’s Interim Final Rule is effective as of May 17, 2021, and public comments are due July 16, 2021. U.S. Treasury guidance may be clarified consistent with the final rule.

[2] In order to expedite payments, U.S. Treasury issued initial payments under an existing ALN, 21.019, assigned to the Coronavirus Relief Fund. If a local unit received funds under this number, it should update its systems and reporting to reflect the new ALN 21.027 for Local Fiscal Recovery Funds.

Waste or Abuse

Report Fraud

Waste or Abuse