Official Site of The State of New Jersey

Official Site of The State of New Jersey

Follow-Up Report – Township of Irvington: A Performance Audit of Financial Management Practices

- Posted on - 03/7/2024

Honorable Tony Vauss, Mayor

Township of Irvington

Irvington Municipal Building

1 Civic Square

Irvington, New Jersey 07111

Re: Follow-Up Report – Township of Irvington:

A Performance Audit of Financial Management Practices

Dear Mayor Vauss:

On March 4, 2009, the Office of the State Comptroller issued Irvington Township: A Performance Audit of Financial Management Practices (2009 Audit),[1] in which we made recommendations to address various identified weaknesses in the Township’s financial management practices. Pursuant to N.J.S.A. 52:15C-11, we conducted a follow-up review to assess the implementation of the recommendations contained in our 2009 Audit. Our findings and conclusions were set forth in a report (2011 Review)[2] issued on November 30, 2011. That report concluded that the Township of Irvington (Township) had not fully implemented 13 of our 21 recommendations. More recently, after communicating with the Township and reviewing audit reports, we elected to perform an additional review of the Township’s financial management practices as part of our monitoring process. The results of our review are set forth below.

Background, Scope, and Objective

Our 2009 Audit examined financial management practices at the Township, identified deficiencies, and made 21 recommendations for improvement. The deficiencies included flaws in the preparation, maintenance, and reconciliation of accounting records; internal control weaknesses related to financial reporting and accounting; failure to comply with laws pertaining to timely filing of financial documents; as well as inadequate personnel practices. Our 2011 Review found 13 recommendations not fully implemented.

We initiated this review (2023 Review) to assess the implementation of recommended improvements to the Township’s financial management and personnel practices since 2011. The COVID-19 emergency caused difficulties in both requesting and obtaining information from the Township. We performed the 2023 Review between August 2021 and July 2023 and included documentation from 2017 through 2023.

Methodology

We performed our 2023 Review to monitor the implementation of recommendations identified as not fully implemented in our prior reports. This 2023 Review focused on issues determined to be significant to the transparency, oversight, or accountability of the Township’s fiscal management and personnel practices. Issues considered less significant were discussed with management and were not part of our review. This review focused on four categories: preparation, maintenance, and reconciliation of accounting records; design and implementation of internal controls; personnel practices; and compliance with laws pertaining to financial administration.

To accomplish our objectives, we reviewed relevant statutes, regulations, and other supporting documentation. We obtained and reviewed publicly available information, including the Township’s annual financial statements, annual debt statements, budgets, and independent auditor’s reports for calendar years (CY) 2017 through 2021. We utilized the Government Accountability Office’s Standards for Internal Control in the Federal Government, or “Green Book,”[3] to provide a framework for our assessment of the Township’s internal controls.

Additionally, we interviewed Township personnel to understand changes in operations related to the preparation, maintenance, and reconciliation of accounting records; the design and implementation of internal controls; personnel practices; and compliance with laws pertaining to financial administration.

Summary Conclusion

Our 2023 Review found that the Township made little progress in implementing the remaining recommendations. Our review found that the Township failed to:

- Maintain accounting records as required by N.J.A.C. 5:30-5.7;

- Implement adequate internal control policies and procedures for financial reporting;

- Conduct effective employee evaluations on a timely basis;

- Produce required financial information accurately and on a timely basis;

- Ensure that the Chief Financial Officer (CFO) had an active Municipal Finance Officer Certificate[4] as required by N.J.S.A. 40A:9-140.13; and

- Identify and prevent contractual relationships that create conflicts of interest between the Township and its officers and employees.

The Township must take appropriate action to strengthen its internal controls and improve its current practices in order to achieve greater operational effectiveness and improve compliance with applicable laws and regulations. The Township must ensure its employees maintain the requisite certifications for their positions. Further, the Township must stop procurement practices that create clear conflicts of interest between the Township and its employees. These practices expose the Township to possible fraud, waste, or abuse through self-dealing or collusion.

In the 14 years since the release of our 2009 Audit, the Township failed to realize the substantial positive impact from fully implementing all of our recommendations. We make seven recommendations to improve the Township’s operations and its compliance with applicable statutes and regulations. It is imperative that the Township takes immediate action.

In addition to the recommendations in this report, we are referring possible ethics violations to the Local Finance Board within the Department of Community Affairs, Division of Local Government Services (DLGS) for their determination of any actions regarding violations of state ethics requirements.

In addition to the recommendations and referral, and in accordance with N.J.S.A. 52:15C-11(b), we provided notification to the Governor, the President of the Senate, and the Speaker of the General Assembly of Irvington’s failure to comply with a plan for corrective action. In light of Irvington’s continued failure to adhere to the law and to implement measures to responsibly manage taxpayer funds, we recommend that the DLGS install a state fiscal monitor to ensure that Township officials come into compliance with corrective actions.

Criteria

N.J.A.C. 5:32-2.1 establishes the duties of the CFO of a municipality. Those duties include the accurate preparation, maintenance, and reconciliation of accounting records; the development and implementation of a system of internal controls to safeguard assets and monitor compliance; and compliance with laws pertaining to financial administration.

N.J.S.A. 40A:9-140.13 and N.J.A.C. 5:32-2.2 prohibit the appointment or reappointment of a municipal CFO without a municipal finance officer certificate issued by the Director of the DLGS. N.J.A.C. 5:32-2.4 establishes that the renewal of a municipal finance officer certificate must occur every two years subject to the applicant’s fulfillment of continuing education requirements, submission of the application, and payment of a $50 fee. An individual may apply within six months of the expiration of the individual’s certificate in the same manner as a renewal. Additionally, the director may extend this period to 12 months after the expiration of the certificate in the event of a natural disaster or medical issue. An individual who holds a municipal finance officer certificate and fails to renew shall be required to apply to take the qualifying examination and pay a fee to obtain a new municipal finance officer certification.

N.J.A.C. 5:30-5.7(b) establishes that all local units, such as municipalities and counties, are required to maintain a general ledger for their current fund and establishes standards for the proper maintenance of the general ledger. The general ledger is required to provide a summary of all financial transactions as recorded in the books of original entry, using a double entry, self-balancing accounting system with the general ledger facilitating the preparation of the financial statements. The general ledger, along with the original books of entry and supporting subsidiary ledgers constitute the complete accounting system. The DLGS issued Local Finance Notice (LFN) CFO 2003-14[5] in November 2003 to reinforce and update the procedures for maintaining a general ledger accounting system. The LFN provided guidance that the application of the standards should extend to all funds. The Local Finance Board recently adopted amended regulations[6] to codify the guidance in LFN 2003-14 and require that all local units maintain a general ledger for all funds.

State statutes require municipalities to prepare financial information, submit the information to the DLGS, and make information available for public inspection. This process provides transparency to taxpayers and facilitates state and local oversight of the Township’s finances. The completion dates of these requirements vary based upon the year-end of the local government. The Township operates on a calendar year basis and is thus required to meet the submission dates in Figure 1.

Figure 1 — Financial Documents Submission Dates

| Financial Document | Statutory Due Date | Statute |

|---|---|---|

| Annual Debt Statement | January 31 | N.J.S.A. 40A:2-40 |

| Annual Financial Statements | February 10* | N.J.S.A. 40A:5-12 |

| Adopted Budget | March 20* | N.J.S.A. 40A:4-10 |

| Annual Audit | June 30* | N.J.S.A. 40A:5-4 |

| * Due dates are subject to extension by DLGS | ||

The Green Book provides a framework for internal control systems for public entities. The Green Book establishes five components of an internal control system: control environment, risk assessment, control activities, information and communication, and monitoring. The five components include 17 principles that support the effective design, implementation, and operation of an internal control system.

The control environment is the foundation for an internal control system. It provides the discipline and structure to help an entity achieve its objectives. A well-designed control environment includes a commitment to integrity and ethical values; oversight of the entity’s internal control system; establishment of an organizational structure; assignment of responsibility and delegation of authority to achieve the entity’s objectives; and performance evaluations and a way to hold individuals accountable for their internal control responsibilities.

The governing body and management should lead by example, demonstrating the organization’s values, philosophy, and operating style. The governing body and management set the “tone at the top” and throughout the organization by their actions.[7] Tone at the top can be either a driver of or a barrier to an effective internal control system. The lack of a strong tone at the top to support an internal control system may result in an incomplete identification of an entity’s risk, inappropriate risk responses, improperly designed or implemented control activities, poor communication, and ineffective monitoring and remediation of deficiencies.[8]

Monitoring Results

Preparation, Maintenance, and Reconciliation of Accounting Records

Our 2009 Audit and 2011 Review identified weaknesses in the processes related to the preparation, maintenance, and reconciliation of accounting records. Our 2023 Review found that the Township failed to implement sufficient corrective actions to ensure the accurate preparation, maintenance, and reconciliation of accounting records.

Reports from the Township’s independent auditor for CYs 2017 through 2021 disclosed that the Township has a computerized general ledger for all funds. However, the auditor repeatedly reported findings related to the maintenance of the general ledger and related accounting records:

- The general ledger for all funds did not agree with various subsidiary ledgers. Specifically, cash receipts recorded to the accounting system contained numerous errors and did not agree with department turnover reports or bank reconciliations.

- The Township failed to accurately record cash disbursements.

The Township’s failure to maintain accurate accounting records has negatively affected taxpayers. The Township reported $789,210 in “unidentified expenditures” in its 2019 annual audit. According to the auditor, the Finance Department transferred expenditures to the grant fund from the 2019 municipal budget. The grant fund reflects the fiscal activity related to federal and state grant programs. However, it appears that the Township did not charge salaries and wages of $661,350 and other expenses of $127,860 to any appropriated federal, state, or local grants. These actions circumvented budgetary controls over spending designed to promote accountability and assist in the prevention and detection of fraud, waste, and abuse of taxpayer funds. In its 2022 budget, the Township included $789,210 under an appropriation for “Expenditures W/O approp. – Grant Fund 2019” to recover the cost of the grant fund expenditures made in 2019 from taxpayers.

The DLGS directs that all municipalities maintain a general ledger for all funds as an essential element of the local unit financial accounting system. N.J.A.C. 5:32-2.1(a)(3) establishes that the Township’s CFO is responsible to ensure the proper and accurate preparation, maintenance, and reconciliation of accounting records.

We urge the Township to implement improvements to its processes related to the preparation, maintenance, and reconciliation of accounting records to comply with DLGS guidance and N.J.A.C. 5:32-2.1(a)(3), remediate audit findings, promote greater transparency, and enhance oversight.

Design and Implementation of Internal Controls

Our 2009 Audit and 2011 Review identified weaknesses in the design and implementation of the Township’s internal controls related to financial administration. Our 2023 review found that policies and procedures related to key aspects of financial administration and reporting were still insufficient. Additionally, the governing body and management employees, such as the Business Administrator and CFO, failed to remediate known deficiencies within its system of internal controls.

Management, including the Business Administrator and CFO, should implement control activities through policies and design control activities to achieve objectives and respond to risks.[9] The Township provided its policies and procedures related to accounting, budget, and the tax collection for our review. Our review identified weaknesses related to accounting and budget policies.

The accounting policies and procedures provided simply list the steps needed to perform a bank reconciliation. The document fails to identify the employees responsible for completing and reviewing the bank reconciliations and the expected completion date. The Township has developed a procedure to track the status of its bank reconciliations; however, the documentation provided indicated that, as of September 2021, three accounts had not been completely reconciled for the year. We requested and received additional documentation indicating that as of the end of January 2023, the Township had reconciled all but two of the reported accounts through December 2022. The two remaining accounts were reconciled through October 2022 and November 2022, respectively. The timely completion of many of the account reconciliations indicates some improvement in the account reconciliation process. However, the Township must make additional improvements to ensure the timely reconciliation of all Township bank accounts.

The budget policy included the Township ordinance establishing their budget process and checklist to guide monthly and year-end financial reporting. The Township completed the checklist for 2021. However, the checklist lacked sufficient detail, did not require evidence of the completion of each step, and was not specific to the Township’s processes. The individual steps on the checklist contain a high-level description of the required action, such as “Post Tax Levy,” but the checklist does not include details such as where to obtain the tax levy or a description of the journal entry needed to enter the levy into the accounting system. Our review of the checklist found no supporting documentation providing evidence of the accurate completion of each step. The checklist contained evidence of review – an employee initialed and dated each section. However, the review did not lead to the correction of an identified deficiency noted on the checklist. The checklist had a check next to the step to tie the Grant Budget Account Status Report to the grants appropriated balance on the Township’s general ledger. The checklist also included a note indicating that the work in that area was not complete. Our 2023 Review found that the 2021 general ledger reported appropriated grant reserves that were $3.8 million dollars higher than the detailed balances reported on the Grant Budget Account Status Report. This variance indicates that the checklist step was not complete and further substantiates our conclusion that the checklist lacks sufficient detail in order to be effective. For the checklist to be useful, the Township must take corrective action to fix errors and unexpected variances when identified.

N.J.A.C. 5:32-2.1(a)(8) requires the CFO to develop and implement a system of internal controls to safeguard assets and monitor compliance. Five consecutive independent audit reports, from 2017 through 2021, identified material weaknesses in the area of internal control over financial accounting and reporting. A material weakness is a deficiency, or a combination of deficiencies, in internal control that result(s) in a reasonable possibility that the system of internal control will not prevent or detect and correct a material misstatement of the financial statements on a timely basis.

The members of the governing body are required by N.J.A.C. 5:30-6.5(b) to familiarize themselves with the contents of the annual municipal audit and certify that they have personally reviewed and are familiar with the “Comments and Recommendations” section of the annual audit. Management should remediate identified internal control deficiencies on a timely basis.[10] The material weaknesses reported in audit reports for CYs 2017 through 2021 indicate that management, including the governing body, failed to remediate known internal control deficiencies on a timely basis for five years.

We urge the Township to implement improvements to its internal controls related to financial reporting to address the material weaknesses noted in its annual audit reports.

Personnel Practices

Our 2009 Audit and 2011 Review identified weaknesses in personnel practices. Although the Township had policies and procedures related to personnel practices, our 2011 Review identified instances of noncompliance with those practices. The 2011 Review also found that the Township had made improvements to its personnel practices since the 2009 Audit. We found evidence that management has developed job descriptions, taken appropriate action when employees did not satisfactorily perform their responsibilities, and partially implemented annual performance evaluations.

Our 2023 Review of annual performance evaluations identified instances in which the Township failed to complete a timely evaluation and inconsistencies between numerical performance evaluation ratings and supervisor comments. A finance employee received a rating of “highly effective,” which indicates consistently demonstrating acceptable performance in fulfilling job functions, despite comments that indicated frequently missed work deadlines. Another finance employee received an overall rating of “highly effective” despite documented concerns regarding the employee’s attendance and use of unauthorized overtime. Clear communication and transparency are important components of employee feedback that help limit misinterpretation and confusion.

We urge the Township to continue to enhance its personnel practices in order to improve the consistency and timeliness of its annual performance evaluations.

Compliance with Laws Pertaining to Financial Administration

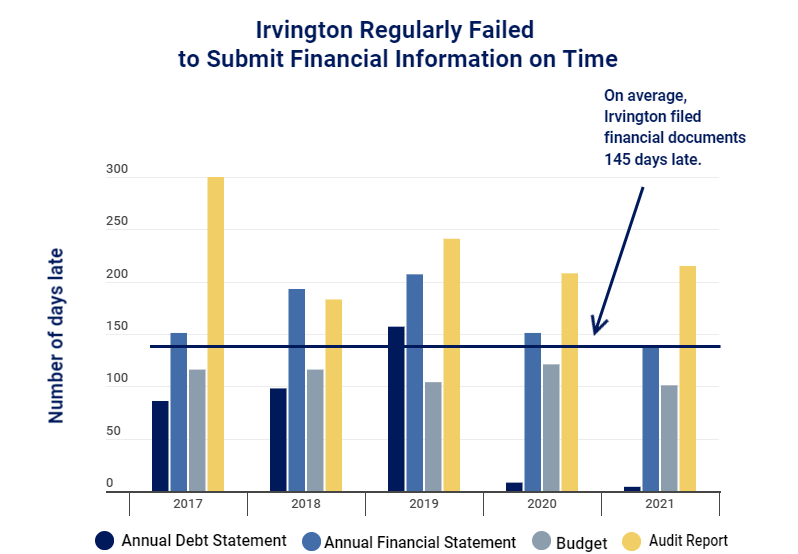

Our 2009 Audit and 2011 Review identified that the Township failed to submit timely financial information. Our 2023 Review found the continued failure to file required financial information on schedule.

N.J.A.C. 5:32-2.1(a)(9) establishes the duty of a CFO to ensure compliance with all statutes, rules, regulations, and directives pertaining to financial administration and such other duties assigned by law to the CFO. State statutes establish mandatory filing deadlines for the reporting of certain financial information that may be subject to an extension by the DLGS. The DLGS issues LFNs to communicate deadline extensions to municipalities. Our 2023 Review found that the Township failed to file required financial documents on a timely basis. The delayed filing of important financial information decreases transparency and limits oversight of the Township’s finances.

Figure 2 demonstrates the historical trend of late filings over the last five years, from CYs 2017 through 2021. On average, the Township filed statutory reports 145 days, or approximately five months, late.

Figure 2 — Late Filings 2017-2021

We urge the Township to implement improvements to its processes to comply with statutory or DLGS-extended filing dates and promote greater transparency and oversight.

Municipal Finance Officer Certificate

Our 2023 Review found that the CFO, who has been employed by Irvington since at least 2009, had an expired municipal finance officer certificate as of December 31, 2022. The certificate became inactive after a statutory six-month grace period as of July 1, 2023. As of September 20, 2023, the DLGS reported that the CFO’s certificate was reinstated after expiring and becoming inactive for the third time in 2020 and informed the CFO that the certificate would not be reinstated a fourth time. The CFO certificate renewal process ensures that municipal CFOs with active certificates complete the required training to maintain their skills and inform them of industry-wide changes. The expiration of a municipal CFO certificate may be cause for removal under N.J.S.A. 40A:9-140.8(b). We note that the Township’s CFO obtained a new municipal finance officer certificate through examination on December 6, 2023.

Conflict of Interest

Local Government Ethics Law (Ethics Law)[11] prohibits local government officers, employees, and immediate family members of an officer or employee from having an interest in a business organization or engaging in any business, transaction, or professional activity that is in substantial conflict with the proper discharge of the officer or employee’s duties in the public interest. The Ethics Law defines an interest as the ownership or control of more than ten percent of the profits, assets, or stock of a business organization. The Township Municipal Code Article 1, § 7-4 similarly prohibits an officer or employee in the government from direct or indirect interest in any contract or job for work or materials, or the profits thereof, to/from the Town. Despite the prohibition in the Township code, the purchasing manual anticipates Township orders from businesses owned by Township employees or their families and requires obtaining at least three quotes. The Township increases its susceptibility to fraud, waste, and abuse by creating situations in which an employee’s duty to the Township and taxpayers conflicts with the employee’s self-interest as business owner.

The CFO’s financial disclosure statements for 2017 through 2023 document an ownership interest in a company that owns a property in the Township. The company leased the property to the Township. The property currently houses the Township’s Office of Community Development and Planning. The Township awarded lease agreements to this company totaling $207,900 for the period July 2017 through June 2022. The annually awarded leases increased from $39,900 for the period July 1, 2017 through June 30, 2018 to $45,000 for July 1, 2021 through June 30, 2022. The CFO’s company submitted documents to the Township in May 2022 as part of the Township’s bid process for the lease of office space for the period July 1, 2022 through June 30, 2023. The CFO submitted and signed the bid documents in his capacity as Managing Partner of the company. The resolution authorizing the contract for office space from July 1, 2022 through June 30, 2023 reported that the CFO’s company was the only bidder. The resolution also indicated that the Purchasing Agent and Municipal Clerk received and opened the bid, the Township reviewed the bid in accordance with Local Public Contracts Law, and the Township Administrator recommended that the Township award the contract to the CFO’s company. Finally, the resolution authorized the award of the contract for $46,000 for the lease of office space to the CFO’s company, directed the Township Attorney to prepare the contract, and reported that the CFO provided the required certification of availability of funds for the contract.

Our review of the procurement documents confirm that the company has leased space to the Township for seven years and that the CFO and a member of the Township Board of Adjustment have an ownership interest in the company that is greater than ten percent. This relationship creates a clear conflict of interest between the personal interest of an employee and the interests of the governing body or taxpayers. The contract provides a substantial disincentive for the CFO to seek out and recommend options that could provide greater benefit to the public, such as buying a property instead of leasing one or consolidating office space into existing Township buildings. This financial relationship is not consistent with the requirements of Ethics Law or the Township Municipal Code. The Township should discontinue the contract as soon as possible in a fiscally prudent manner that minimizes the disruption of any essential Township services.

In its response to a draft copy of this report, Irvington disputed our conclusion that a conflict of interest exists. Irvington referenced N.J.S.A. 40A:9-22.5 and stated that it “indicates that a local authority shall not award a contract that is not publicly bid.” We note that the section referenced is applicable to independent local authorities, not the municipality itself. Further, Irvington also suggested that the CFO does not have a role in the decision-making process. We note that the CFO is a local government officer, files an annual financial disclosure statement,[12] certifies the availability of the funds, and is responsible for compliance with statutes pertaining to financial administration. We disagree with Irvington’s position and are referring this matter to the Local Finance Board for its determination regarding violations of state ethics rules.

Recommendations

- Comply with statutory and regulatory requirements for the prompt completion and submission of financial information.

- Take all necessary action, which may include staffing changes or the hiring of consultants, to correct known deficiencies and eliminate recurring audit findings.

- Perform a formal review of the Township’s policies and procedures related to accounting and financial reporting. Design and implement detailed policies and procedures to address known deficiencies and comply with statutes and regulations.

- Provide training to ensure consistent and effective employee evaluations.

- Perform a review of Township fiscal operations to determine if the current staff and staffing levels are appropriate to meet the Township’s needs. Hold employees accountable who fail to meet the requirements of their job titles or Township goals through evaluations and appropriate disciplinary measures.

- Identify all Township positions that require an employee to hold a license or certificate. Obtain copies of all valid certificates or licenses for Township records. Take disciplinary action, as necessary, in the absence of a valid certificate or license.

- Develop a process to identify vendors that have the potential to create conflicts of interest between the Township and its employees and officers. The Township should discontinue contracts that create conflicts of interest as soon as possible in a fiscally prudent manner that minimizes the disruption of any essential Township services.

Reporting Requirements

We provided a draft copy of this report to the Township for its review and comment. The Township did not comment on certain sections of our report and disagreed with our conclusion related to Ethics Law. Its response was considered in preparing our final report and is attached as Appendix A.

By statute, we are required to monitor the implementation of our recommendations. To meet this requirement, within 90 days, the Township shall report to our office regarding the actions that have been or will be taken to address the unresolved issues in this report. Additionally, given the 14 years since the release of our 2009 Audit and the limited progress in implementing our recommendations, we direct the Township to submit written updates regarding its compliance with our recommendations every 90 days thereafter until further notice.

We thank the management and staff of the Township for the courtesies and cooperation extended to our auditors during this review.

Sincerely,

KEVIN D. WALSH

ACTING STATE COMPTROLLER

By: Christopher Jensen, CPA

Director, Audit Division

[1] Available at: https://www.nj.gov/comptroller/news/docs/090304_audit.pdf.

[2] Available at: https://www.nj.gov/comptroller/news/docs/irvington_follow_up_report_11302011.pdf.

[3] UNITED STATES GOVERNMENT ACCOUNTABILITY OFFICE, STANDARDS FOR INTERNAL CONTROL IN THE FEDERAL GOVERNMENT (SEPT. 2014), (“Green Book”), https://www.gao.gov/assets/gao-14-704g.pdf.

[4] This report uses the term “municipal finance officer certificate” to describe the professional credential required of municipal CFOs in New Jersey. However, documents we reviewed also refer to this credential as “New Jersey Certified Municipal Finance Officer License” or “Certified Municipal Finance Officer Certificate.”

[5] LFN CFO 2003-14, https://www.nj.gov/dca/divisions/dlgs/lfns/03/cfo-2003-14.pdf.

[6] 55 N.J.R. 1690(a), (Aug. 7, 2023).

[7] U.S. GOVERNMENT ACCOUNTABILITY OFFICE, Green Book at 22.

[8] U.S. GOVERNMENT ACCOUNTABILITY OFFICE, Green Book at 22.

[9] U.S. GOVERNMENT ACCOUNTABILITY OFFICE, Green Book at 9.

[10] U.S. GOVERNMENT ACCOUNTABILITY OFFICE, Green Book at 9.

[11] N.J.S.A. 40A:9-22.1 to -22.5.

[12] The requirement for filing annual financial disclosure forms applies only to "local government officers". https://www.nj.gov/dca/divisions/dlgs/programs/ethics_docs/93-0022.pdf.

Waste or Abuse

Report Fraud

Waste or Abuse